By Nick Baughan, Managing Director, Marks Baughan*

I’ve been advising legal technology founders and investors on M&A, capital raising, and strategic financing decisions since 2003. Twenty-three years and 130 transactions later, I can say with certainty that we’ve never seen a more exciting time in legal tech than now.

The reason is AI, and the opportunity has never been bigger. Here’s how AI is changing the game for all the key players on the field and creating a $1 trillion prize.

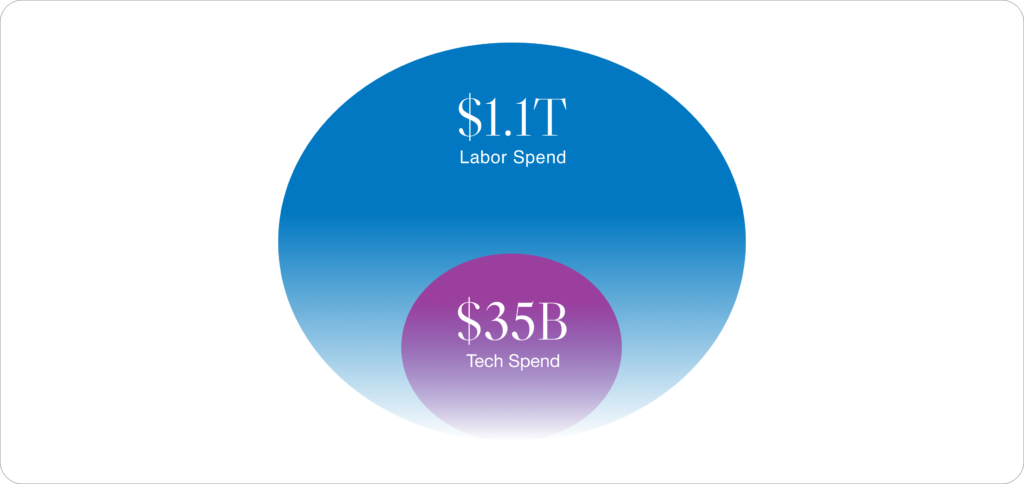

From a $35B Market to a $1T Opportunity

The sale of software to law firms and corporate legal departments is a $35 billion market. The provision of legal advice and associated legal services is a $1.1 trillion market. That’s a 30x TAM expansion. This pivot from tech spend to labor spend has driven an unprecedented wave of investor interest in legal tech over the past two years — all powered by AI.

AI is capable of automating work that was previously done by lawyers and legal staff, meaning technology vendors can now compete for a share of the $1.1 trillion spent on legal labor, not just the $35 billion spent on legal software.

A quotation from Andreessen Horowitz succinctly articulates the reframing of this market opportunity: “Legal is the infrastructure for capitalism.” If legal is a load-bearing pillar of our economy, then legal tech isn’t just software for lawyers. It’s technology that upholds commerce and society. As we move from tech spend to labor spend, investors are recognizing this new position for legal tech and re-valuing it accordingly.

To understand where this is headed, it helps to map the four major forces currently shaping the market.

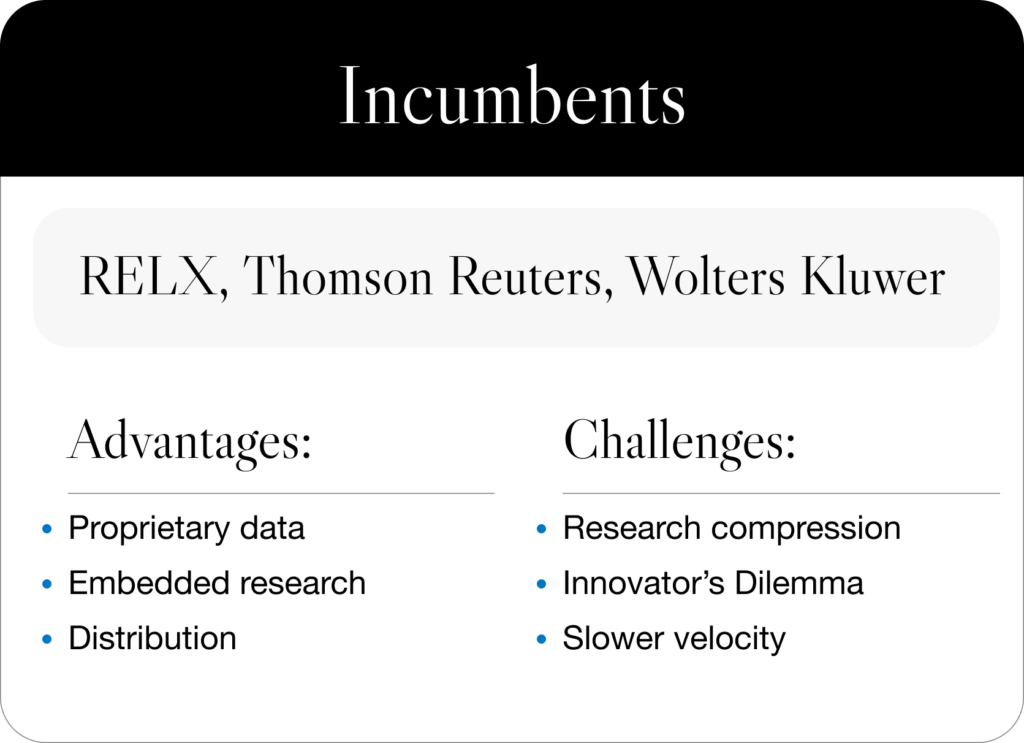

The Players: Incumbents — the Original “Intelligence Vendors”

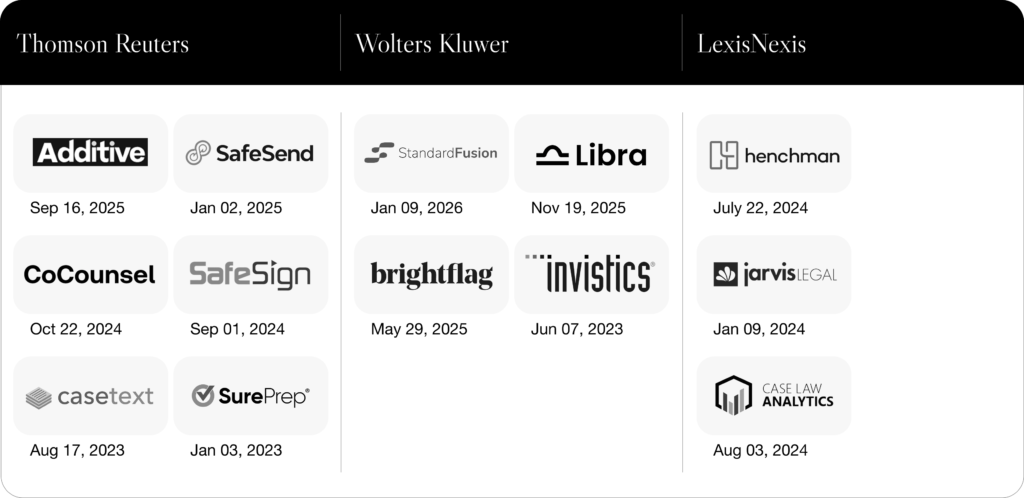

The three largest traditional legal tech players — RELX (LexisNexis), Thomson Reuters, and Wolters Kluwer — built their empires on proprietary content databases refined through decades of editorial work. Their consistent M&A strategy over the past 20 years has been to protect and enhance the value of that data by deepening the moat around their datasets and expanding the use cases for them. That’s why their acquisitions have focused on adding breadth of content and buying software workflows that port content directly to users’ desktops.

These are wildly profitable businesses. They don’t need to grow more than 2% – 3% a year, but they cannot shrink. They also can’t innovate quickly. Like any large corporate entity, they struggle with the Innovator’s Dilemma, and every technology cycle forces them to make acquisitions to keep pace. We saw it with Thomson Reuters and Casetext, and we’re seeing it again now with AI-focused bolt-ons across all three players.

Thomson Reuters’ CEO Stephen Hasker stated in February 2026 that the company deployed $850 million into M&A in 2025 alone, with more inorganic activity under assessment. He also stated in August 2025 that Thomson Reuters has $12 billion to spend on M&A through 2028. These players will remain among the most acquisitive in the market. Expect them to continue buying content, software, and AI capabilities to protect their dominant market positions.

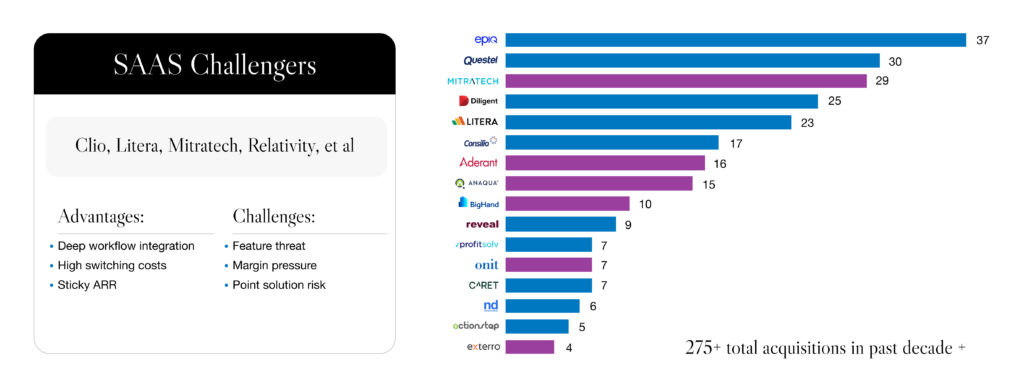

The Players: Private Equity-powered SaaS Challengers — Workflows and Systems of Record

If I had to name the most significant exogenous force in legal tech over the past 20 years before AI, it would be private equity.

Over the past 15+ years, the private equity sector has run a highly effective playbook on aggregating vertical market software sectors. The blueprint involves buying on-premise, perpetual license software businesses, migrating them to the cloud, generating recurring revenues from a SaaS licensing model, and then consolidating fragmented industries to add scale. Legal tech is no exception.

The above image depicts 16 of the most acquisitive private equity-backed legal software players in the market, spanning every part of the legal ecosystem. Collectively, they’ve completed over 275 acquisitions in the past 10-12 years — building formidable, embedded platforms that scale from $50M to over $1B in ARR. While they face headwinds in the age of AI, they are extremely well-capitalized and will continue to be acquisitive in both software and AI to round out their AI capabilities.

A Note for Founders on Private Equity

Founders tend to have their valid concerns about recapitalization transactions with private equity firms where they sell 70-80% of their company and have to give up complete control. But Marks Baughan has advised countless founders who have done very well in partnering with private equity in this way. Bringing on a partner that can help you identify acquisitions and give you capital to accelerate sales or product development is a powerful wealth creation strategy. It’s not uncommon to see the value of reinvested equity at the time of an initial recap ultimately exceed the cash taken off the table.

It’s also worth noting that the average deal size completed by the group of companies in the image above runs $50 – 75 million. For many founders, that’s life-changing money. A founder who has kept their cap table lean has options: they can raise more capital at a $50 – 100 million valuation, or they can sell at that level for life-changing money. Either way, they retain full flexibility. A founder who locks themselves into a Series B at a $300 million valuation has to go down an exit path approaching $1 billion. It’s smart to consider that type of risk and weigh the money and flexibility of an earlier, more conservative funding round or sale against it.

The Players: VC-fueled AI Disruptors — Agentic Outcomes

What we’ve seen in venture capital over the past two years is extraordinary. In 2025 alone, there were approximately 300 Series A or later transactions in legal tech with total volume exceeding $6 billion. We’ve never seen this volume of VC activity or this caliber of venture firms entering the space.

This enthusiasm is a strong signal of investor interest in the pivot from tech to labor spend. In the image below are eight companies that have raised the most money at the highest valuations.

Consider Harvey, currently valued at $11 billion having raised nearly $1 billion. If investors are targeting a 3x return, they’re underwriting a $30+ billion exit. Scale that math across these disruptors, and you arrive at nearly $100 billion in expected exit value from companies that, for the most part, didn’t exist two years ago. For context, the combined market cap of Wolters Kluwer, Thomson Reuters, and LexisNexis is approximately $130 billion.

Many of these companies have now been valued well beyond what a traditional incumbent can absorb in an acquisition. That means a wave of IPOs is coming. We expect to see a new leadership class of highly valued public legal tech companies emerge over the next two years. For founders, that translates into a growing set of well-capitalized strategic acquirers and potential partners.

The Players: Large Language Models — Powering the Stack or Moving Up It?

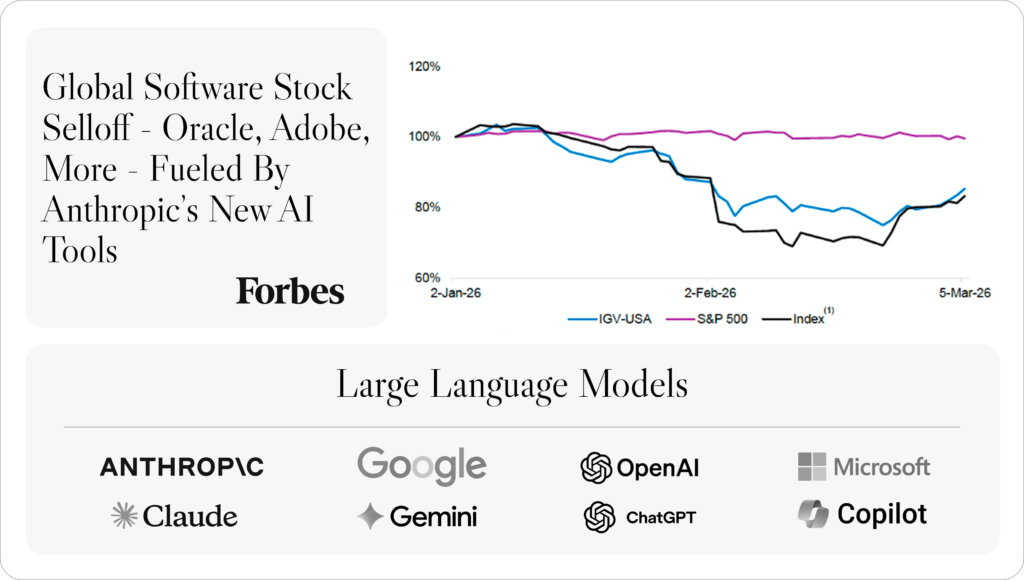

On February 3, 2026, markets shook when Anthropic announced that its AI tool, Claude, had a plug-in for the legal market. Shares of legal data incumbents and software vendors fell sharply on fears that LLMs intended to enter the application layer directly. Since then, Anthropic has walked back its stated intentions. Stocks have partially recovered, but many remain down 20–40% on the year from those fears.

No one fully knows where the LLMs want to compete or what their long-term monetization strategies are. Will they remain below the stack and just sell intelligence capabilities to the vertical market vendors? Or will they enter and compete in the stack?

One thing is certain: these players will have outsized influence on legal tech’s M&A landscape for the next several years.

We’re also seeing — so far, at least — that these players aren’t trying to compete directly with the incumbents. The early picture is one of integration: Anthropic partnering with Intapp; iManage partnering with both Harvey and Legora; LexisNexis integrating Harvey; Microsoft embedding Harvey into its stack. The LLMs, the incumbents, and the workflow software players are currently leveraging each other’s core capabilities. The stack is integrating, not collapsing.

The dynamic of this ecosystem remains fluid. These are some of the most powerful technology companies ever built, and their long-term competitive boundaries are unknown.

The New Playing Field: Four Forces, One Massively Expanding Market

These four groups of players are converging around a $1 trillion+ opportunity, and for now, they need each other. Their interdependence is creating an extraordinary moment for founders.

The TAM has expanded by 30x. Incumbents are actively acquiring. Private equity platforms are continuing to buy at high volume. Record VC funding is creating a new class of buyers that will need to consolidate and scale. And the public markets are preparing to welcome a new generation of legal tech leaders.

There has never been a better time in legal tech, whether you’re building or exiting. Think carefully about your cap table and know that the buyers for your business have never been more numerous or better capitalized. The $1 trillion wave in legal tech is cresting right now.

*Nick Baughan is Managing Director at Marks Baughan, a global investment bank in the legal and compliance industries. He first presented these remarks at the LTH Velocity conference in New York on March 9, 2026.